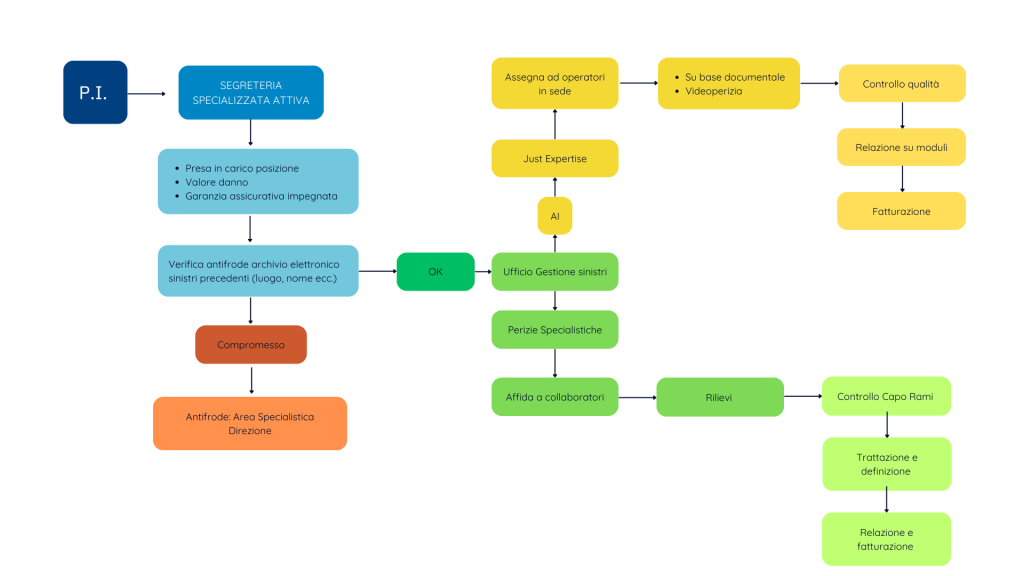

PaceIngegneria is organized with a proactive centralized administrative office that receives assignments from throughout the territory and interfaces with the Company and the Client ensuring timely first contact.

segreteria@paceingegneria.it

Branch managers assign tasks to individual employees by territory and expertise.

tecnico@paceingegneria.it

Le risultanze di tale attività vengono riportate alle Compagnie nei format richiesti.

Each employee is trained to understand from the first contact the expectations and needs of the insured to meet which he or she takes action directly and/or through in-house professionals.

The development of expertise goes through emergency management i.e., participation in recovery and safety works, determination of causes, assessment of damage and its contractual settlement. Cause investigation and damage determination are entrusted to professional engineers always internal to the PaceIngegneria structure. The added value of this structure lies in the participation in the process of the best professional figure necessary to perform the " expertise" namely the engineer.

Our surveyors are on the ground ready to make a geo-localized photographic and video documentation of damages and causes, and our Surveyors are also connected online for compatibility verification, determination of damages , application of CGAs, and settlement of the damage through liquidation or compensation in specific form.

Technical time for position management 50 min

Ancillary time to agree with the insured on the availability of places and interview for negotiation, definition and payment 24 h

Savings on average appraisal cost for values up to 1,500.00 euros up to 50 percent

Decrease in the average time to complete the 'assignment 80%.

Our surveyors are on the ground ready to make geolocated photo and video documentation of damage and causes

Our Surveyors are connected in real time for damage determination and compatibility verification based on the surveys performed

Only the study from 'inside these Companies performed by PACEINGEGNERIA to respond to the directional order allowed the writer to monitor materials , structures and procedures realmenti useful for the restoration according to the' emergency hypothesis of intervention underlying the title of the new claim.

Such work has contributed since the 'time to mortify the lump sum claims even for small areas to be treated that initially stood at 1950.00 euros until the current 600.00 euros or so. The entire insurance market has benefited from this, but it has been diverted by the fact that the new agreements, if on the one hand they made them accept lower base amounts over time, have slowly allowed the decrease of the areas admitted to the minimum value of direct settlement. From the 'era to the present, there have been various players in the market who have organized themselves by issuing concessions and contracts with entities and municipalities to provide them with this service at zero cost in exchange for an assignment of their credit from insurance claims generating uncontrolled diseconomy on the basis of borderline agreements and expenses.

We have been successfully countering this phenomenon for more than 15 years through centralized settlement that levels counterparties and favors the entry of the market rule for determining costs in a policy of reducing disbursements by Insurance Companies also enhancing the economy of scale that is generated due to the large number of claims handled by these Road Cleaning Companies. Even today, many players in the settlement of damages have not started this virtuous path generating distortions in the settlement world that always generate new counterparties attracted by high earnings and ease of file processing and speed of settlement.

It remains a hope that the market of insurers will begin to read between the lines of this phenomenon, limiting the benefits of fast settlement to only those cases that affect the community, according to the provisions of the Environmental Law. In this way we can 'get a sudden downsizing to reality' of the costs of these restoration interventions that have nothing to do with the 'emergency.